Interest Rates? Lock in Now or Wait a Couple of Weeks? (loan, 2015)

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

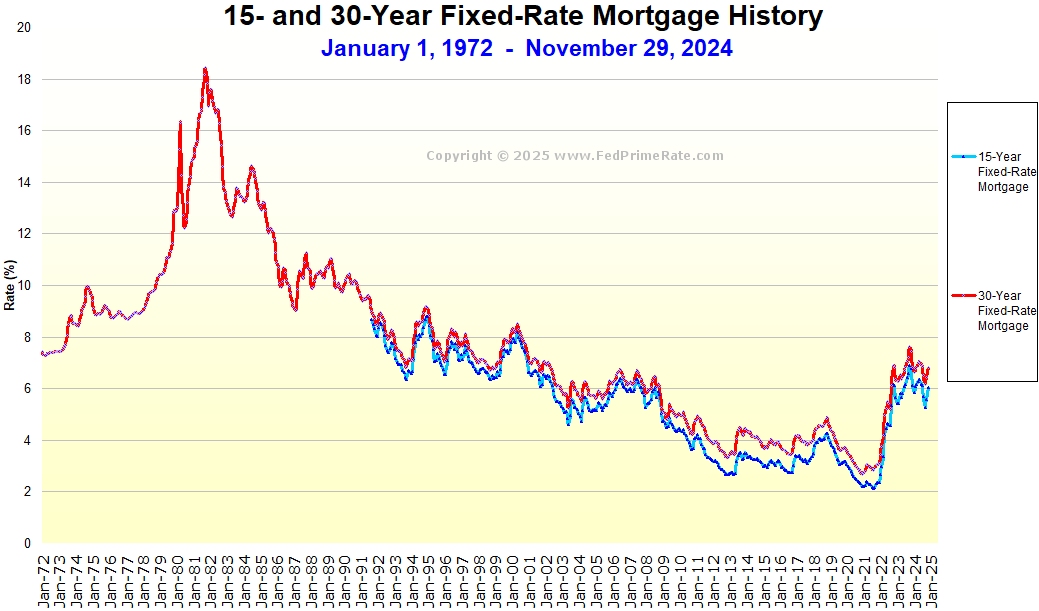

Do we think interest rates are going to continue to climb into September or will they come down? Complete insanity that they are headed toward 8% and there are still bidding wars on homes! Nonetheless, I need a small mortgage, so should I lock in or wait a couple of weeks? Could rates possibly increase???

Don't screw around - lock. 33% chance it will go down, 33% chance it will stay the same, 33% chance it will go up. So 66% it will stay the same or get worse.

This is a different lending environment. Lenders are losing money on loans. Many are hoping you actually do not come to them (on certain products). Two years ago, lenders were rolling in cash. Today, they are stretched for cash. And, now auditors are going through all those loans from 2021 and 2022 and calling out and forcing these same lenders to buy back loans they do not like...........or pay 5% penalty. It's not going to take much to tip the cow on small and mid-sized lenders/banks.

Borrowers are out there shopping lenders' rates without a property to even lock in. Hey there, I can lock you in at 6%!!! I also have a bridge or two for sale.

Different environment than even 6 months ago. Lock or lose.

My neighbor just told me his interest rate is 2.9 percent. I wonder how many of those loans are out there and how much the banks are losing because of those deals?

I worked at a bank 40 years ago and every morning on the loudspeaker, the Prime Rate was announced. I remember the day it was announced at 20%. You could have heard a pin drop; everyone was stunned.

A co-worker was very excited to have gotten a mortgage for a house with a 9.5% interest rate. We were all so happy for him.

ARMs are no longer a good option. They used to be a way of getting into the market but the banks are losing so much money on those 2.5 percent loans that they have to make it up. An ARM is almost as expensive as the initial 30-year rate.

I just giggle when there’s all this hand wringing over rates “heading for 10%.” In 1984 I had a one year adjustable rate loan that was about 12 or 13%. I refinanced a different mortgage in the early 90s and went from 10% to 8% and thought I had died and gone to heaven.

If you weren’t a homeowner in the 80s you don’t know mortgage rate pain.

Please register to post and access all features of our very popular forum. It is free and quick. Over $68,000 in prizes has already been given out to active posters on our forum. Additional giveaways are planned.

Detailed information about all U.S. cities, counties, and zip codes on our site: City-data.com.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.