Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

I live in Houston, Texas and am looking at my medicare options.

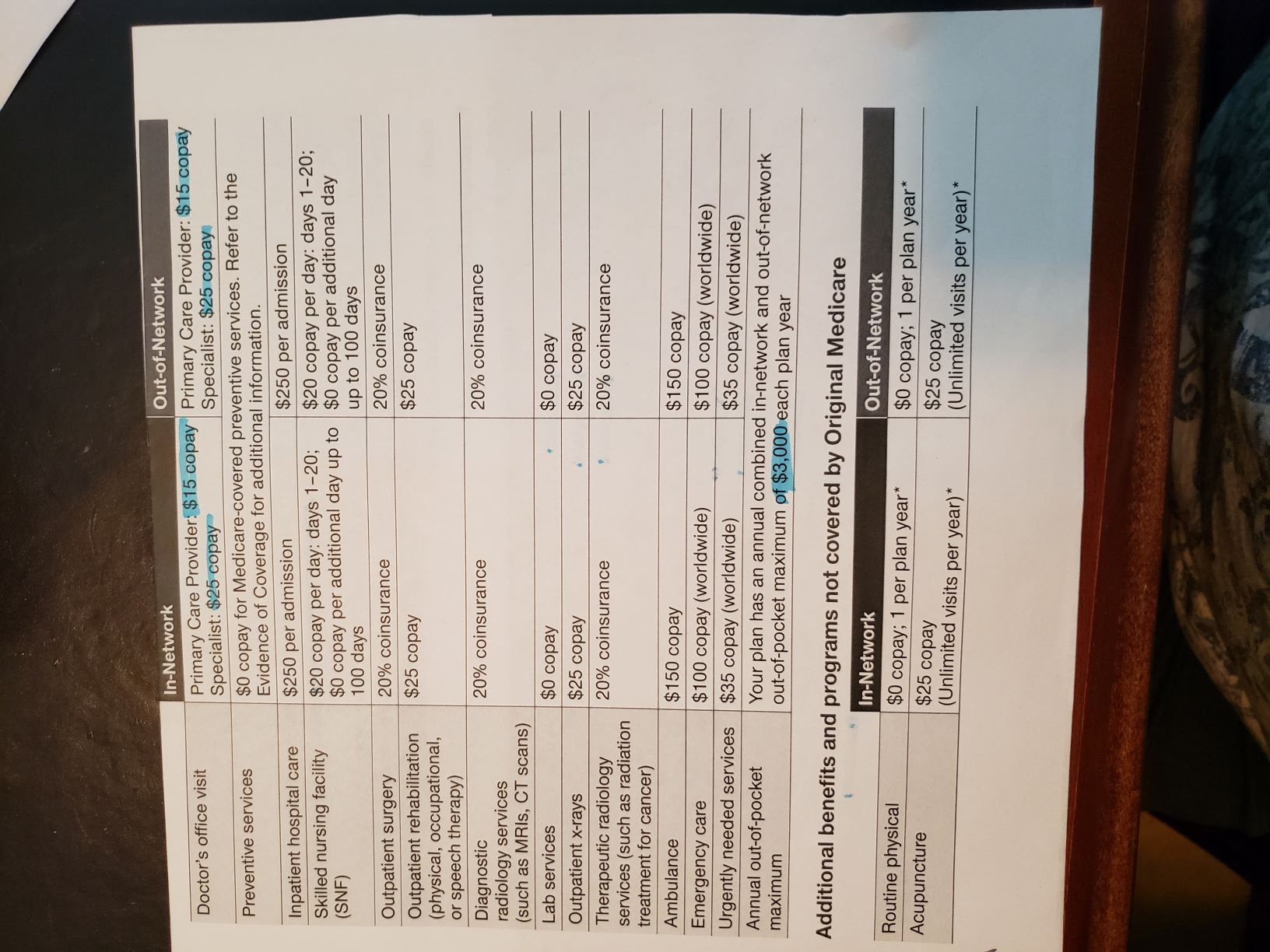

I have a company advantage plan available that looks pretty good. It charges $60 a month and has no upcharges for out-of-network providers. It has a $3000 out-of-pocket max. The unknown is the cost of the 20% coinsurances. It looks very good to me for today. But, I worry about future needs. Of course this plan can change over the years and not be as attractive.

I'm leaning towards a supplement G and am comparing companies. I want to consider rate increase history. I was advised by a broker that the United Health Care (AARP) policy is really not the best option because they try to make you think you are getting a big break on premium by discounting a high rate. The other companies have the lower rates without having to offer a discount. The first year for me on UHC would be $136 and would increase 3% each year for ten years until the discount disappears. Then there would also be a general increase each year. Also, from my dad's experience, UHC raised rates twice this year.

The broker has liked Aetna in the past, but says that ever since CVS bought them, they have had higher increases than prior to CVS. I don't know if they are playing catch-up to the rest of the industry, or if this will continue unabated. Aetna premium for me would be $129.

As an alternative to Aetna, he pushes a subsidiary of Mutual of Omaha called United World Life Insurance. It's premium would be $134. I've read a few bad comments about MOO on this forum. I don't know if this applies to United World Life.

I then called to ask about USAA supplement G and learned that their premium would be about $140. I was told told that they review prices once a year and that some years they have decreases. They only have history on F because they've only recently started offering G.

It may be that all Texas policies are attained age. I'm not sure about this.

Your broker is misrepresenting AARP UHC. Most people on this board have or are purchasing AARP UHC - and are very happy with it. Yes, rate increases occur twice a year - once for age and once for inflation - but after age 77 increases only occur due to inflation in medical costs - not age.

AARP UHC is the ONLY policy which is community-rated in most states which do not mandate community-rating (and that is MOST of them). Which means age-based rate increases CEASE at age 77. UHC does discount rates for those under age 77. Thereafter, whether one is 97 or 77, the base rate is the same. This not true for any other company, many of which continue age-based rate increases to age 85, MOO (and its subsidiaries) among them. Live long enough with an MOO or other attained age policy, and your premiums could easily be well over $400/month. That is not an exaggeration. MOO is the worst.

Attained-age companies establish new subsidiaries/entities in order to open new books of business - as risk pools are often closed after four years locking existing policyholders into an increasingly older and sicker risk pool which, of course, results in much higher rate increases.

I wouldn't consider an attained-age full Medigap policy from any company, least of all MOO or any of its subsidiaries - unless I was in a guaranteed issue state or a state like CA, MO, OR where one can change to another Medigap without health underwriting either on anniversary of policy or your birthdate. Texas is not such a state.

If you want excess coverage, AARP UHC Plan G is the way to go. Otherwise, its Plan N also works well for many people.

This issue has been discussed extensively on this forum on many threads, among which are:

The Health Exchange Company has been providing different plans and healthcare supplements check this out

aetna medigap

mutual of omaha provider

cheapest medicare supplement plan f

mutual of omaha medicare supplement rates

Clearly you read none of what OP wrote - or my response - or any of the links included in my responses. The foregoing quote is of no help whatsoever to OP . Cheapest Medigap supplement is almost always not the best choice UNLESS one is considering a high-deductible F. That, too, has been discussed in the above links.

I live in Houston, Texas and am looking at my medicare options.

I have a company advantage plan available that looks pretty good. It charges $60 a month and has no upcharges for out-of-network providers. It has a $3000 out-of-pocket max. The unknown is the cost of the 20% coinsurances. It looks very good to me for today. But, I worry about future needs. Of course this plan can change over the years and not be as attractive.

I'm leaning towards a supplement G and am comparing companies. I want to consider rate increase history. I was advised by a broker that the United Health Care (AARP) policy is really not the best option because they try to make you think you are getting a big break on premium by discounting a high rate. The other companies have the lower rates without having to offer a discount. The first year for me on UHC would be $136 and would increase 3% each year for ten years until the discount disappears. Then there would also be a general increase each year. Also, from my dad's experience, UHC raised rates twice this year.

The broker has liked Aetna in the past, but says that ever since CVS bought them, they have had higher increases than prior to CVS. I don't know if they are playing catch-up to the rest of the industry, or if this will continue unabated. Aetna premium for me would be $129.

As an alternative to Aetna, he pushes a subsidiary of Mutual of Omaha called United World Life Insurance. It's premium would be $134. I've read a few bad comments about MOO on this forum. I don't know if this applies to United World Life.

I then called to ask about USAA supplement G and learned that their premium would be about $140. I was told told that they review prices once a year and that some years they have decreases. They only have history on F because they've only recently started offering G.

It may be that all Texas policies are attained age. I'm not sure about this.

Any thoughts?

Terry

You left out a few details- are you female or male? Med Advantage is PPO? Since you said that you have out of network benefits. What is your hospital copay like? Do you have any dependents on this company policy?

$60/mo does seem reasonable, but I am curious what your hospital copays, spec, PCP copays, rx benefits are like?

You should always ask if you are able to return to this insurance if you go elsewhere.

Please keep in mind that u would have to buy Part D plan in addition to Supp.

As you are aware, you have opportunity to change at Annual Election. Some Med Supp companies offer GI in leaving employer group coverage, whether voluntary or involuntary.

I read a lot of the posts on this board yesterday and recognized your expertise. I'll check the links you provided too. Indeed, I may have seen some of them. I wrote my new post to see if anyone had any thoughts on these companies. Thanks for your input.

I think the whole process stinks that you have to essentially pick a company now for unknown future needs and that we get locked in. And I hate to give up my company plan. I keep going back in forth about whether I should go with company PPO (Which is essentially not a PPO because non-network charges are the same as network charges) or Medigap G. I understand that I can get a new window for no underwriting if I should decide to leave my company plan. But, that's a crap shoot too. I think I'm talking myself into G. N is inexpensive, but I'd worry about the excess charges.

So, it's a matter of finding the right G plan. I think most plans in Texas are attained age. The UHC plan stops the discounts at age 77. It does seem like a tricky way to do age increases (vanishing discount). But it might pay off in the long run. UHC also said they'd pay 50% of my gym membership.

I'm still perplexed though. My dad moved from NY to FL at age 88 and was able to switch from his advantage plan in NY to his F plan in FL . His broker has told me that his UHC F plan had 2 general increases so far in 2019. She had suggested he change carriers this year, but I know he would not be able to pass underwriting.

You left out a few details- are you female or male? Med Advantage is PPO? Since you said that you have out of network benefits. What is your hospital copay like? Do you have any dependents on this company policy?

$60/mo does seem reasonable, but I am curious what your hospital copays, spec, PCP copays, rx benefits are like?

You should always ask if you are able to return to this insurance if you go elsewhere.

Please keep in mind that u would have to buy Part D plan in addition to Supp.

As you are aware, you have opportunity to change at Annual Election. Some Med Supp companies offer GI in leaving employer group coverage, whether voluntary or involuntary.

Female

Ppo, but not really (see my next reply)

Just me

I did ask about returning. Normally you can. But I'm a surviving spouse of my husband's plan, so no.

Edited to add: So, it's called an advantage PPO plan, but I can use any doctor that accepts medicare and I pay the same.

Edited to say: Double click and the images are rotated correctly.

Edited to add: So, it's called an advantage PPO plan, but I can use any doctor that accepts medicare and I pay the same.

Edited to say: Double click and the images are rotated correctly.

If I were you, I would NOT get out of that coverage unless it just doesn't have a good network. Those are VERY RICH benefits as today's retiree plans go. Your hospital copay is ONLY $250/stay!, low PCP/spec, Skilled Nursing- only $20/day beyond day 20 instead of $174, Max out of pocket on your drugs with $0 deductible plus it even throws in Personal nursing care (which is not a core Medicare benefit). As you said, you would pay 20% on diagnostic and outpt surgery, but those would be based on 20% of a contracted rate. You didn't mention if there is Max Out of Pocket for hospital/medical expenses, but even better if you have one (which you should).

Even if you stayed up to the next Open enrollment period, Texas law will allow you to enroll in a Med Supp Guaranteed Issue situation when you involuntarily or voluntarily leave the retiree coverage.

Put it into perspective:

$140 - 60 = $80/mo savings x 12 mos = $960

Part D plan ~ $25/mo x 12 = $300

reaching Part D deductible for non brand name rx- $410, low cost for generics, but brands would not be cheap.

Would the $250 hospital include whatever surgeries one might have while there? It appears like it would.

This also includes silversneakers that I can use at more than one gym.

I'm wondering about a big illness....I live in MD Anderson's backyard and I'd want to make sure I could use them if it comes down to that. I like the $3000 out of pocket max on all the non-drug expenses. And a separate OOP max of just under $3000 for drugs.

eterry2 - your broker didn't mention USAA because that company does its own sales, not through brokers.

As of last year, USAA offered Silver Sneakers with its Plans G and F which is a nice plus.

It uses a combination of attained age and community pricing to establish premiums. Ask USAA customer service for some rate sheets to see how it would compare to UHC at various ages.

USAA is a top insurance company so it's worth a good look.

Please register to post and access all features of our very popular forum. It is free and quick. Over $68,000 in prizes has already been given out to active posters on our forum. Additional giveaways are planned.

Detailed information about all U.S. cities, counties, and zip codes on our site: City-data.com.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.